16 Oct 2020

Grafiek van de Week Fidelity: Chinese groei-aandelen zitten nog niet aan plafond

Beste redacteur,

Net als op veel andere markten doen de groeiaandelen in China het momenteel beter dan de waardeaandelen. De voorsprong van groeiaandelen heeft zelfs een nieuw record bereikt, zo blijkt uit de Grafiek van de Week van Fidelity International. Volgens de vermogensbeheerder zullen de Chinese groeiaandelen overigens nog een tijd de overhand houden, ook al is de winstgevendheid van de Chinese maakindustrie recent sterker hersteld dan verwacht.

Hieronder vindt u het volledige bericht:

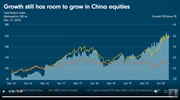

Chart Room: Why growth still has room to grow in China equities

This week’s Chart Room shows the valuation premium for China growth stocks versus value stocks recently hit a new all-time high, lifted by outperformance in the consumer, tech and healthcare sectors. Investors may be wondering whether it’s time for a style rotation, given China’s stronger-than-expected recovery and improving industrial profitability, which tend to support value. Despite this, we think the growth rally still has room to grow.

As in many markets elsewhere, value stocks in China have been outpaced by growth stocks. Recently, the case for value has been bolstered by the strong recovery in China’s industrial profitability, with policy support lowering operating costs, and early signs of an acceleration in producer prices, with petroleum-related sectors helped by the rally in oil prices. But questions remain over the durability of this momentum.

More recently, the initial inventory re-stocking of energy resources and industrial metals appears to have run its course, and a recovery in producer prices is far from guaranteed. That’s partly because external demand still appears weak if we strip out exports of medical equipment. This situation is unlikely to improve as the number of new Covid-19 cases outside of China continues to rise.

Meanwhile, China’s recovery in domestic demand is also underwhelming in some respects. Retail sales have turned positive year-on-year and the property sales are strong, but this largely reflects an easing of credit conditions to support the economy through the pandemic. And the People’s Bank of China seems to be turning more cautious on monetary policy, which could tap the brakes on the recovery.

A sustained reflation of China’s economy that supports a rotation from growth to value stocks can only be achieved if demand growth matches the increase in industrial output. So far, that does not yet appear to be the case. Growth likely still has room to grow.

Notes to editors

Voor meer informatie:

Stampa

Patricia Boon +31(0) 20 404 2630

fidelity@stampacommunications.com

This material is provided to you in your capacity as media agency/journalist. The material serves exclusively as background information. Rewriting of content is under your responsibility unless otherwise agreed.

Powered by Onclusive PR Manager © 2026